The financial television channel CNBC has hit hard times. Nielsen ratings show the network’s viewership is at a 21 year low. This is a far cry from two decades ago. The dot-com bubble of the late 90s and early aughts gave the channel its highest ratings in history. The Federal Reserve’s easy money flooded the market, hitting blue chip stocks like a tidal wave. All of a sudden laypeople fancied themselves market gurus, playing the market and investing for a big pay day some time in the future. Trader and commentator Barry Ritholz described the environment as one where “CNBC was everywhere.” “Gyms, bars, restaurants, any public place you went into that had a TV — even sports bars! — had the ticker strewn channel running in the background.”

The financial television channel CNBC has hit hard times. Nielsen ratings show the network’s viewership is at a 21 year low. This is a far cry from two decades ago. The dot-com bubble of the late 90s and early aughts gave the channel its highest ratings in history. The Federal Reserve’s easy money flooded the market, hitting blue chip stocks like a tidal wave. All of a sudden laypeople fancied themselves market gurus, playing the market and investing for a big pay day some time in the future. Trader and commentator Barry Ritholz described the environment as one where “CNBC was everywhere.” “Gyms, bars, restaurants, any public place you went into that had a TV — even sports bars! — had the ticker strewn channel running in the background.”

One bubble burst and a financial crisis later, the home of hothead Jim Cramer has cooled off significantly. There are a few reasons for this. As Lehman Brothers cratered into bankruptcy, the middle class saw its 401(k)s lose a significant portion of value. Such a loss begged for an explanation. Yet economists and financial experts were caught off-guard by the crisis. No popular orator of the dismal science could explain why the banking system devolved into chaos. CNBC’s most popular hosts and guests could only offer guesses.

One person was the exception: Peter Schiff. The internet video “Peter Schiff was right” collaged all of Euro Pacific Capital founder’s dire warnings about the housing bubble. At the time, he was ridiculed on air. Schiff was a cassandra, spouting crank theories long disproven by economic orthodoxy. But by September of 2008, he had the last laugh. The financial world was in turmoil, and Schiff’s explanation - based on the Austrian school’s theory of boom and bust cycles - was at last seen as legitimate.

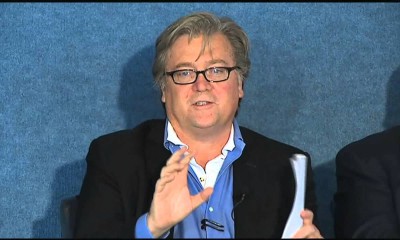

But memories can sometimes be short. Half a decade later, and Schiff remains the Rodney Dangerfield of finances. Thanks to a flawed call on consumer price inflation and the price of gold, he still finds himself the joke of many a CNBC broadcasts. His continued warnings about the Fed’s reckless inflation binge and coming dollar crisis provide plenty of excuses for the channel’s on-air personalities to pick on him. On a recent edition of “Futures Now,” Schiff was challenged on his inaccurate assessments of macro-economic trends. Scott Nations of NationsShares called him out on his dour Fed assessment. Nations piled on the contempt, practically questioning how Schiff has a career in investment at all. Exasperbated, Schiff proclaimed, “I am wrong a lot less often than most people on this program… and all you do is hassle me.”

Schiff’s rant doesn’t immediately come off as exonerating; let alone mature. He sounds childishly bitter - entitled to respect for his prescient forecasting. This behavior is not admirable in any setting. Anyone who demands praise for his achievements is treading on shaky ground. Pride before the fall, and all that.

Still, Schiff has a point. He went on national television and endured a deluge of mockery for challenging established opinion. His forecasts, while not always correct, were far more accurate than those of his contemporaries. No one likes an ideologue wedded to a philosophy to the point of redundancy; yet there comes a point when facts are facts. When it mattered, Schiff had both an accurate assessment of the economy and a solid explanation to justify his findings. His advice might have saved the livelihood of millions, had it been taken. To this day, his call was seen as heroically prophetic, even while his philosophical underpinnings are still held in suspicion. He hasn’t earned the benefit of the doubt in the eyes of his Keynesian-minded contemporaries.

The lack of respect - and even off-putting attitude - showed toward Schiff can be blamed on outright bias. Like any thought-sport, there is accepted doctrine and kooky theories. The winning team is naturally suspicious of anyone who challenges their earned position.

When it comes to mainstream economics, Keynesianism reigns supreme. Central banking is widely viewed as a benefit to the economy; not a meddling danger. The orthodoxy is enforced by believers of what James Grant calls the “PhD standard.” The financial press loves the idea of a few select men guiding the economy toward peak employment. Reporters and commentators need to stay in the good graces of decision-makers to boost their own career. No one would know who Jon Hilsenrath of the Wall Street Journal is if it weren’t for his close contacts to Federal Reserve officials.

Schiff’s Austrian-minded approach to markets is a challenge to acceptable opinion, and he pays the price by burning at the stake on television. The Keynesian revolution didn’t just bring the idea that economies can be fine-tuned with the help of central planners; it brought a high-minded smugness to economic science. It taught aspiring dictators that with enough math formulas and aggressive authority, they could be gods among men. Such conceit is paid for in economic depressions, prolonged unemployment, broken family life, and general societal malaise. The misery wrought by the Keynesians consensus is paramount. Yet it’s practitioners seem immune to considering the simple proposition that their worldview could, in any way, be flawed.

Presumption, though attractive, leads to folly. Lives and fortunes have been lost in the gamble known as the stock market because of the hubris built into economic assumptions. You might think that being caught off guard by the biggest banking crisis in 80 years would force observers to show more respect toward an outsider like Peter Schiff. But then you might think that the Keynesianism belief in turning one dollar into several by spending it at the local department store is the stuff of fantasy.

Economic forecasting is a dangerous job. As Mark Twain put it in his novel Pudd’nhead Wilson, “October. This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.” Every wrong prediction could doom a career, or a bank account. Prudence and humility are the only sound tools for building one’s reputation. The talking heads on CNBC appear to know neither. They pledge allegiance to the flag of the tinkering bureaucracy. It explains the loss of ratings, and loss of confidence in the ability of “experts” to see what’s coming down the tracks. Refusing to learn from mistakes will lead to future blunders. Pundits that don’t heed this message are doomed to fail.

Facebook

YouTube

RSS