While the failure of fiscal policy is widely recognized, monetary policy still enjoys credibility, not only among policy makers but also with professional economists. Yet deeper investigation shows that monetary policy is like shooting in a dark room. Disaggregating the highly aggregated variables of standard monetary economics reveals that monetary policy suffers from a profound pretense of knowledge. When central banks are not able to fulfill their claim and promote economic growth, employment and price stability, the question comes up what the real mission is that they are after. The Federal Reserve System was founded in 1913 with the intention to safeguard the big players of the financial system. After a period when central bankers claimed that they would also promote prosperity we are now back at the old paradigm.

While the failure of fiscal policy is widely recognized, monetary policy still enjoys credibility, not only among policy makers but also with professional economists. Yet deeper investigation shows that monetary policy is like shooting in a dark room. Disaggregating the highly aggregated variables of standard monetary economics reveals that monetary policy suffers from a profound pretense of knowledge. When central banks are not able to fulfill their claim and promote economic growth, employment and price stability, the question comes up what the real mission is that they are after. The Federal Reserve System was founded in 1913 with the intention to safeguard the big players of the financial system. After a period when central bankers claimed that they would also promote prosperity we are now back at the old paradigm.

Monetary expansion

Similar to what has happened in Japan over the past two decades or what is going on in Europe right now, the policy of quantitative easing by the US central bank over the past couple of years has only marginally affected the money supply and even less so the price level. “Quantitative easing†means that the central bank buys government bonds and other assets from the financial sector in return for fresh money, which the central bank creates itself autonomously. This money created by the central bank, the so-called “monetary baseâ€, forms the foundation of the inverted pyramid of money creation in the financial system. The more as there is base money in the financial system, the more additional money can be lend out by commercial banks. Yet as of now not much additional deposit money has been created. Instead of lending out funds to the private sector, banks deposit the new cash at the central bank.

As it is shown by the data of the US Federal Reserve (chart 1), the monetary base underwent an explosion since 2008. From little more than US$ 800 billion, base money increased to almost US$ 2,800 billion. This is amazing in itself, yet even more so when we consider that in the decades before this upturn the monetary base showed only tiny regular increases. Even during the inflationary times of the 1970s and the boom years of the 1990s the expansion of the monetary base was moderate compared to what happened in the past few years.

Chart 1 - US monetary base

Before the onset of the current crisis, which has already received the provisional name “Great Stagnationâ€, economists postulated a fairly close link between the expansion of the monetary base and the other broader monetary aggregates and central bankers pronounced the arrival of the “Great Moderation†as the result of the increased sophistication of monetary policy.

For the monetarist school in particular it was the central bank that held the key to the money supply. Milton Friedman launched monetarism with the verdict that the US central bank “caused†the Great Depression because it did not sufficiently expand the money supply in the 1930s. As can be seen in the chart below (chart 2), US money supply in the form of M2 is still pretty much on the same trend line as it began in the mid-1990s. The enormous expansion of base money did not show up in a similar expansion of the money supply.

Chart 2 - US money supply M2

While the banking sector is awash with money in the form of base money there is relatively little increase in lending to the private sector of the economy (see chart 3).

Chart 3- Commercial and industrial loans at commercial banks

Banks have become more risk-averse and reluctant to lend as much as the private sector disdains from borrowing. Companies are cautious to invest and many families reduce outstanding debt. It is mainly only government that has expanded its borrowing. The extreme expansion of the monetary base did not enter the real economy in the same dimension. Consequently the price level did not rise as much as the increase of the monetary base would indicate (see chart 4).

Chart 4 - US Consumer price index

The immense monetary impulses that were launched by the American central bank over the past five years has had little effect on price inflation and it also did not stimulate economic growth sufficiently in order to lift the level of employment (see chart 5).

Chart 5 - US Employment-Population Ratio

The monetary impulses that came from the central bank in the form of the expansion of the monetary base have failed to expand the money supply and thus there has been no transmission of the stimulus to the real economy and to the price level. Not only did the monetary stimuli have little effect on the money supply, the monetary stock itself has had less impact on economic activity because the so-called “velocity†of money has fallen since the year 2000 and hit new lows since over the past years (chart 6).

Chart 6 - Velocity of Money for M2

The data shown above (chart 1 to chart 6) provide evidence that monetary policy has been ineffective when it comes to economic growth and employment. Of course, one could argue that without such an expansive monetary policy things would be worse and that unemployment would be much higher and one could claim that the economy as a whole would have fallen over the cliff into a deflationary depression without the massive stimulus. However, this line of reasoning is problematic because there is no way to prove this thesis. The point to make is that despite the vast size of the monetary stimulus and even more so because of the fact that together with the monetary expansion launched by the US central bank, the US government has also provided enormous fiscal stimulus packages with an extraordinary surge of US federal government debt (see chart 7), the economy did not take off.

Chart 7 - US Federal Government Debt

Once again we are confronted with a situation which confirms what the Austrian school of economics has proclaimed since the beginning of the 20th century that the very same policies which have provoked the outbreak of the crisis cannot be the same to fight the crisis. The Austrian business cycle theory asserts that artificial booms are the result of an overly expansive monetary policy that sets the interest rate below its natural level. Pushing the interest rate even lower in the bust is not the right cure because it helps to postpone adaptation to the new conditions and thus will prolong the time for recovery to come. While monetary policy authorities declare the promotion of economic growth, employment and price stability as their prime mission, they actually are the prime source for the recurrent stagnation, unemployment and inflation.

What’s Behind the Facts?

Once again, as the data show, monetary economics is confronted with the fact that in economic matters there are no stable quantitative relationships in place. Macroeconomic correlations between aggregates that may have held for decades can break down not only abruptly but also in an extreme way. As it is shown by velocity of the M2 money stock (chart 6), the frequency of monetary transactions has been increasing for decades before it took a dramatic turn towards contraction at the turn of century. As is also confirmed by the rise and fall of velocity in the 1970s and 1980s, rising inflationary expectations tend to accelerate velocity, while disinflationary or deflationary expectations lead to a reduction of the velocity of money. Behind the variables lies human action, and human beings are able to learn and and to change their expectations and goals. Neglecting this fact limits severely the possibility of a “science of monetary policy†and explains why this approach has such a poor predictive record. Some of the explanations that are put forth as new insights to explain what appear paradoxical in the view of mainstream economists are actually old hats for those scholars who work in the tradition of Austrian Economics. Austrian economists have always rejected a mechanistic interpretation of the quantity theory of money. That monetary policy has re-distributional effects and that the credit volume matters – propositions that caused some stir recently at the Jackson Hole conference of central bankers – are one of the earliest tenets of the Austrian school of economics. It is with these caveats that monetary analysis should be made and it is then that the quantity theory of money will offer a useful guide to disentangle the complexities of money and monetary policy.

The basic equation of exchange at the heart of quantity theory of money as it was formulated in its modern version by Irving Fisher states the identity (for a critique see Rothbard 2004) between the money stock (M) and the frequency or velocity (V) with its turnover for transactions (T) at average prices or the price level (P). Substituting transactions by real output (Q) and accordingly modify the price level (P) and velocity for nominal national income, we get the modified equation of exchange which would equate money (M) multiplied by its velocity (V) with nominal income (Y).

M.V≡T.P

M.V≡Q.P≡Y

In this form the equation also shows that the velocity of money circulation (V) is the quotient between national income (Y) and the money stock (M). Conventional Keynesian macroeconomics defines national income (Y) as the sum of expenditures for consumption goods (C), investment goods (I), government (G) and net exports (NX). Yet this high aggregation hides the fact that any of these expenditures is the result of a quantity and price component. Consumption expenditure (C), for example, is actuallyt C = pc . qc and so on for the rest of the aggregates. Expenditures have a price (p) and quantity (q) component and for economic analysis it is calamitous if this difference remains hidden as it is the case in the standard Keynesian framework. Likewise we must disaggregate the left side of the equation into the monetary base (MB) and the banking multiplier (mb) as the determinants of the money stock (M), whereby the banking multiplier (mb) reflects the reserve ratio (r) in the financial sector and thus in how much of a given quantity of base money (MB) will be maintained at the banks as reserves (R).

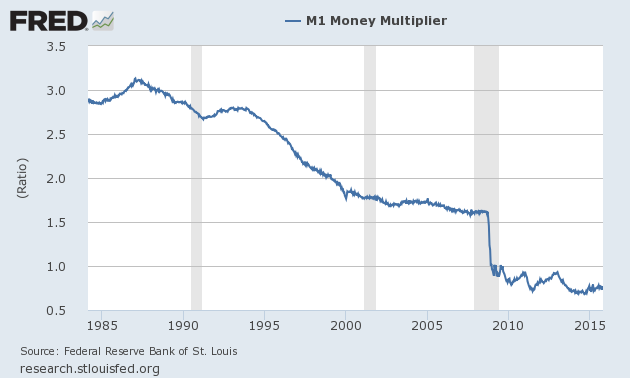

The less reserves (R) are held as a fraction of demand deposits (D), the lower the reserve ratio (r) and the higher the banking multiplier (mb). When banks reduce lending, fewer deposits will be created. The reserve ratio rises while the multiplier shrinks and with it the money supply will be smaller. As it is shown in the figure below (chart 8), the multiplier for the narrow monetary aggregate M1, which includes mainly currency in circulation and demand deposits at financial institutions has been falling since the late 1980s and took a free fall during the latest recession (shaded area in chart 8).

Chart 8 - M1 Money Multiplier

The definition of national income (Y) by its components of consumption (C), investment (I), and government spending (G), as it is done by the Keynesians, is actually just one way of many to define which factors determine aggregate expenditures. By focusing on these three components, the Keynesian approach ignores he structure of production, i.e. the fact that the national product as an aggregate is composed of a myriad of different products. What is being purchased is not consumption or investment but specific individual consumption and investment goods. This way a further disaggregation (see Garrison 2000) is warranted with the additional extension that money is not only used to buy goods and services as they get registered in the national income statistics but also to acquire financial assets.

In order to understand what lies behind this phenomenon it is necessary to disaggregate the variables and differentiate between the “money side†(MV/P) and the “goods side†(Q) of the equation of exchange.

MV=QP

MV/P = Q

The monetary aggregate M consists of the monetary base (MB) multiplied by the banking multiplier (mb), which leads to:

(MB . mb . V)/P = Q

As can be seen in this representation of the equation of exchange, the transmission mechanism from the “money side†to the “goods side†of the economy, i.e. depends on the monetary multiplier (mb), the velocity of money (V) and the price level (P). Any of these factors can either neutralize or amplify the initial monetary impulse. Even if the monetary impulse would reach the “goods side†(Q) as intended it is in no way predicable how the structure of production will change as the result of the monetary impulse including changes of the interest rate. It is mainly the monetary base (MB) that is under control of the central bank and which can be managed through the policy rate, which for the United States is the federal funds rate.

In order to accomplish the recent massive expansion of the monetary base (see chart 1), the American central bank had to move its policy interest rate, the federal funds rate to “zero bound†(see chart 9):

Chart 9 - US Effective Federal Funds Rate

It was foremost the collapsing money supply that attracted the attention of the monetarists. However, the basic error of monetary policy today as it was in the Great Depression is not the inactivity of central banking in the slump, but the active stance that was taken at the inception and the continuation of the artificial boom, when central banks lower the monetary interest rates and feel justified by an apparently stable price level. Now, the instigators of the latest episode of an unsustainable boom downplay the risk of hyperinflation and claim that the money and debt creation through monetary and fiscal policy has not gone far enough and that it takes even more new money to bring the economy back to life as it is asserted in the statement of the Federal Open Market Committee of the Federal Reserve System of September 13th, 2012: “To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee agreed today to increase policy accommodation by purchasing additional agency mortgage-backed securities at a pace of $40 billion per month. The Committee also will continue through the end of the year its program to extend the average maturity of its holdings of securities as announced in June, and it is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities. These actions, which together will increase the Committee’s holdings of longer-term securities by about $85 billion each month through the end of the year, should put downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.â€

Pretense of Knowledge

Although the variables in the extended formula of the equation of exchange are not fully independent, their links to central bank actions are rather loose. A monetary expansion or contraction coming from the monetary base can transform the original monetary impulse into various degrees of strength depending on the monetary multiplier and the velocity of circulation, and from there it can affect in different degrees the components on the right side of the equation. The interrelations get even more complex because the performance of the components will also have a feedback on the monetary multiplier and the velocity of circulation themselves. A favorable investment climate that propels the stock market and lifts asset prices will not only induce an increase of the supply of assets but also tends to accelerate velocity of circulation and the banking multiplier. The expansion of the monetary base can affect both the consumer goods and the investment goods, and within the investment goods, it will impact differently on the various stages of production. If expansive monetary policy takes place in an environment of productivity increases or other cost reductions that are strong enough to compensate for the monetary impulses, the prices of investment and consumption goods need not rise in a way that would be proportional to the increase of money as also asset markets can absorb a considerable part of excess liquidity.

Analyzed by the variables of the equation above the monetary impulse from the monetary base can be amplified or nullified depending on the size of the monetary multiplier and the velocity of circulation. Even by assuming a smooth transmission, the question arises as to which degree the different variables will change because of the original monetary impulse when in consequence of the policies human behavior and expectations change. A variation of the monetary base may go into the prices of consumer goods or it may affect mainly the prices of investment goods or the excess liquidity may go into the asset markets. Likewise fiscal stimuli will evaporate when tax credits are used to buy imported goods or to eliminate excess debt. When the main impulse goes to the investment goods, it will affect the various stages of production differently. Here, as with the other two transaction classes, it cannot be determined ex ante how the impulse transmits from prices to quantities. There is also another feedback at work among the transaction classes (consumer goods, investment goods and assets) so that the original impulse that comes from the monetary base will affect the different transaction classes and will have different degrees of feedback on the monetary multiplier and the velocity of circulation. Given that there are no reliable quantitative relations among the variables, central banks are unable to calibrate their policies. There is no certainty as to whether the monetary impulse will affect in a specific way a specific variable. Only in the most general form can it be said that an inflation of the monetary side will affect the goods side.

What then, we must ask is the true mission of central banking as one cannot calibrate the effects of its monetary policy on the real economy and price level? The answer is provided by the historical origin of central banking. As Rothbard and many other authors, for example Lawrence White, have shown, central banking grew out from the cooperation between the state and the big players of the banking sector. The deal that was struck said that the big banks will finance government and the government won’t let the big banks go bankrupt. For that purpose a lender of the last resort was installed in the form of a central bank which would obtain the privilege by the government to produce unlimited amounts of fiduciary money. Over time the various constraints that were in place under the classical gold standard were removed step by step, particularly during the past century. In 1971, with the so-called Smithsonian agreement, the last anchor for the US dollar fell. At the day when President Nixon fully abandoned what was still left of the gold standard, the starting gun was fired for the escalation of the financial sector into its current gargantuan proportions and with the growth of the financial sector government began with the built-up of public debt to its current colossal dimensions. Yet debt accumulation cannot go on forever. As much as there is a boom when debt is expanding, there is a bust time when debt is contracting. These are the big tidal waves of the modern economy and when the tide is changing few things remain how they were. The current crisis shows many sign that indicate that such a change of tides has come.

The mission of modern central banking

What, so we must ask, is a central banking good for when it is not even able to guarantee a stable price level (see chart 10)?

Chart 10 - Purchasing power of the US dollar since the inception of the FED

Why keep a dictatorial creature within the government body that operates differently from other governmental agencies largely outside of public control? Why hold on to an institution that more often than not has failed to provide full employment and price level stability? By these criteria the Fed has indeed been a failure. Yet the verdict will be different if the main objective of modern central banking is not to promote economic growth and full employment in an environment of a stable price level. What if the fundamental task of central banking is to safeguard the financial system? Central banks create money out of thin air and as such they are able to act without a limit as the lender of the last resort. Central banking is an instrument that was put in place in order to protect the big players of the financial market from going bankrupt. It is in this sense that the monetary policy of the US central bank has fulfilled its mission since its inception and has continued doing so over the past couple of years (see chart 11) not much different from what central banks have done in Japan and what they carry out in Europe right now.

Chart 11 - Excess reserves of the US banking system

While central banks are effective as lender of the last resort and thus operate to safeguard the big players of the financial system from going bankrupt, they are not only incapable of promoting economic growth, employment and price level stability, they are in fact the major promoters of the business cycle. Always under pressure to set the interest rate as low as it can get, central banks provoke artificial booms which inevitably must result in a bust. The big players in the financial market can play the game without the risk of going bankrupt as they can bank on their central bank to bail them out. Bernanke and Gertler (2001) argued explicitly that central bankers should not try to prick asset bubbles but to stand ready to bail out banks and financial institutions when the bubble bursts. In his speech as a Governor of the US central bank on “Monetary Policy and the Stock Marketâ€, Bernanke declared in 2003: “The ultimate objective of monetary policymakers is to promote the health of the U.S. economy, which we do by pursuing our mandated goals of price stability and maximum sustainable output and employment. However, the effects of our policy instruments, such as the short-term interest rate, on these goal variables are indirect at best. Instead, monetary policy actions have their most direct and immediate effects on the broader financial markets, including the stock market, government and corporate bond markets, mortgage markets, markets for consumer credit, foreign exchange markets, and many others.â€

Operating as bailout machinery for the financial system, the US central bank has thoroughly infected the monetary system with moral hazard. The Fed has perverted the capitalist system into one where losses get socialized. Not only is the modern monetary system constructed in a way that makes banking artificially extra profitable through the fractional reserve mechanism, the system also allows that executives and shareholder in the banking sector earn excessive remuneration when times are good while the big players also can rest assured that the central bank will safeguard them in the bust. Â

Conclusion

Central banks do not have the tools to bring about economic growth and employment or to maintain price level stability. The monetary transmission mechanism is far too complex to be calibrated in any reliable way. What central banks have under control is the monetary base. With this instrument they hold the key in their hands to create liquidity at will. The main job of central banks consists in protecting the financial system in the bust. Central banks perform this task by providing funds to the major players of the financial sector. While claiming to pursue price level stability and low unemployment, central bankers actually lay the foundation for inflation and mass unemployment. As the creators of excessive liquidity central bankers are the source of the boom and bust cycle and of secular inflation.

Facebook

YouTube

RSS